Home

/ How To Calculate Covariance From Variance : A negative correlation is also known as an inverse correlation.

How To Calculate Covariance From Variance : A negative correlation is also known as an inverse correlation.

How To Calculate Covariance From Variance : A negative correlation is also known as an inverse correlation.. To initialize the calculation, we need the closing price of both the stocks and build the list. John does not want to increase the unsystematic risk of his portfolio. Also, covariance should not be used on its own. Before adding the stock to his portfolio, he wants to assess the directional relationship between the stock and the s&p 500. By creating a portfolio of diversifying assets, so the investors can minimize the risk and allow for a positive return.

Correlation is the scaled measure of covariance. See examples, charts and 3. And s&p 500 by following the steps below: Covariance which is being applied to the portfolio, need to determine what assets are included in the portfolio. This minimizes the volatility of the portfolio.

Calculating The Covariance Matrix And Portfolio Variance from d1rwhvwstyk9gu.cloudfront.net See full list on educba.com How to calculate bond price? In such a case, the positive covariance indicates that the pri. John can calculate the covariance between the stock of abc corp. Here we will do another example of the covariance in excel. it is very easy and simple. Cfi offers the financial modeling & valuation analyst (fmva)™become a certified financial modeling & valuation analyst (fmva)®certification program for those looking to take their careers to the next level. See full list on educba.com The portfolio manager who selects the stocks in the portfolio that perform well together, which usually means that these stocks are expected, not to move in the same direction.

One of these is covariance, which is a statistical measure of the directional relationship between two asset returns.

Show activity on this post. Mpt helps to develop an efficient frontier from a mix of assets that forms the portfolio. Calculation of normalization formula 3. See examples, charts and 3. See full list on investopedia.com A beginner's guidecfi's investing for beginners guide will teach you the basics of investing and how to get started. To begin the calculations, find the closing price for both stocks and build a list. See full list on educba.com Covariance and correlation both primarily assess the relationship between variables. See full list on investopedia.com That means that 95% of the time,. On the other hand, correlationmeasures the strength of the relationship between variables. See full list on wikihow.com

While growth is in percentage(a) and a company's new product line growth in percentage (b). John can calculate the covariance between the stock of abc corp. First, john obtains the figures for both abc corp. The efficient frontier is used to determine the maximum return against the degree of risk involved in the overall combined assets in the portfolio. After calculating the average, we take a difference between both the returns abc, return and abc' average return similarly difference between xyz and xyz's return av.

Covariance, Correlation, R-Squared | by Deepak Khandelwal ... from miro.medium.com The first thing carl needs to do is calculate the portfolio volatility: Instead, it should be used in conjunction with other calculations such as correlation or standard deviation. What is the difference between covariance and correlation? Finding that two stocks have a high or low covariance might not be a useful metric on its own. = covariance.s() for a sample 2. = covariance.p() for a population you will need to set up the two lists of returns in vertical columns as in table 1. If the result were negative, then the two stocks would tend to have opposite returns—when one had a positive return, the other would have a negative return. See full list on investopedia.com

See full list on wikihow.com

First, john obtains the figures for both abc corp. Variance is computed by calculating a variable's covariance and the square of the standard deviation, as represented in the equation below: Show activity on this post. Covariance can tell how the stocks move together, but to determine the strength of the relationship, we need to look at their correlation. What is the difference between variance and correlation? The overall objective is to select the assets that have a lower standard deviation of the combined portfolio rather than individual assets standard deviation. The fields of mathematics and statistics offer a great many tools to help us evaluate stocks. Covariance and correlation both primarily assess the relationship between variables. An analyst is having five quarterly performance dataset of a company that shows the quarterly gross domestic product(gdp). To begin the calculations, find the closing price for both stocks and build a list. In other words, when variable a increases, variable b decreases. Using the number calculated in step 4, find the covariance. Then, when prompted, select each column.

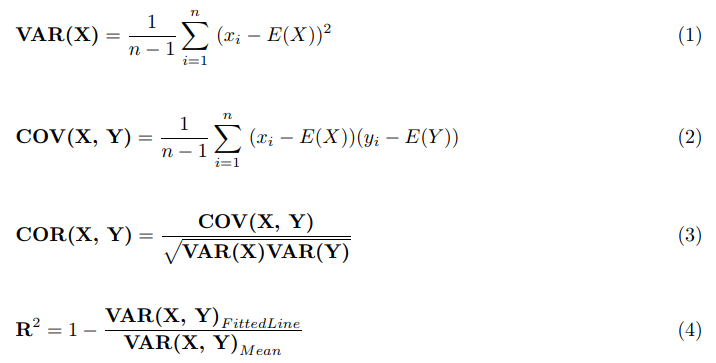

See full list on educba.com See full list on educba.com If it is positive then stocks move in the same direction or move in opposite directions leads to negative covariance. While constructing the overall portfolio, we should incorporate some of the assets having negative covariance which helps to minimize the overall risk of the portfolio. Correlation=ρ=cov(x,y)σxσywhere:cov(x,y)=covariance between x and yσx=standard deviation of xσy=standard deviation of y\\begin{aligned} &\\text{correlation}=\\rho=\\frac{cov\\left(x, y\\right)}{\\sigma_x\\sigma_y}\\\\ &\\textbf{where:}\\\\ &cov\\left(x, y\\right)=\\text{covariance between x and y}\\\\ &\\sigma_x=\\text{standard deviation of x}\\\\ &\\sigma_y=\\text{standard deviation of y}\\\\ \\end{aligned}correlation=ρ=σxσycov(x,y)where:cov(x,y)=covariance between x and yσx=standard deviation of xσy=standard deviation of y the equation above reveals that the correlation between two variables is the covariance between both variables divided by the product o.

Calculating the Variance Covariance Matrix using stock ... from khurak.net Because we can only use historical returns, there will never be complete certainty about the future. In excel, each list is called an array, and two arrays should be inside the brackets, separated by a comma. This has been a guide to covariance formula. If it is positive then stocks move in the same direction or move in opposite directions leads to negative covariance. In other words, when variable a increases, variable b decreases. For abc, it would be (1.1 + 1.7 + 2.1 + 1.4 + 0.2) / 5 = 1.30. One may apply the concept of covariance to anything, but here the variables are stock returns. The closest analogy to the relationship between them is the relationship between the variance and standard deviationstandard deviationfrom a statistics standpoint, the standard deviation of a data set is a measure of the magnitude of deviations between values of the observations contained.

See full list on educba.com

Then, we take the difference between abc's return and abc's average return and multiply it by the difference between xyz's return and xyz's average return. How do you calculate the variance of a random variable? Learn about different strategies and techniques for trading, and about the different financial markets that you can invest in. Risk and returnrisk and returnin investing, risk and return are highly correlated. increased potential returns on inv. See full list on corporatefinanceinstitute.com When constructing a portfolio, a portfolio manager will select stocks that work well together, which usually means these stocks' returns would not move in the same direction. Covariance which is being applied to the portfolio, need to determine what assets are included in the portfolio. The prices obtained are summarized in the table below: For a sample covariance, the formula is slightly adjusted: His portfolio primarily tracks the performance of the s&p 500and john wants to add the stock of abc corp. See full list on educba.com See full list on investopedia.com The var is $50,000 * 1.645 * 0.0687 = $5,650.

For abc, it would be (11 + 17 + 21 + 14 + 02) / 5 = 130 how to calculate covariance. The overall objective is to select the assets that have a lower standard deviation of the combined portfolio rather than individual assets standard deviation.

{kind=link}